A Cost Segregation Study is a federal income tax tool that increases your near-term cash flow in the form of a tax deferral. During a Cost Segregation Study, the parts of your building that qualify for shorter recovery periods are identified, quantified and classified to produce additional depreciation deductions which reduce the amount of tax owed. Depreciation is a deduction that real estate investors can claim on their income taxes each year to help them recover the cost of owning, operating and maintaining that property. By using this strategy, you will reduce the amount of money you owe on your income taxes each year, reducing the expenses of owning investment real estate. Doing this frees up money for other investments or purchases.

The most advantageous time-frame to order a Cost Segregation Study is during the same year after you buy, build or remodel your commercial property. This provides the most tax savings by accelerating depreciation of applicable items. If you did not perform a Cost Segregation Study initially, you can order a look-back study. A look-back study allows you to claim a catch-up tax deduction in a single year. Look-back study on properties are able to be performed on properties purchased, built or remodeled as far back as January 1, 1987.

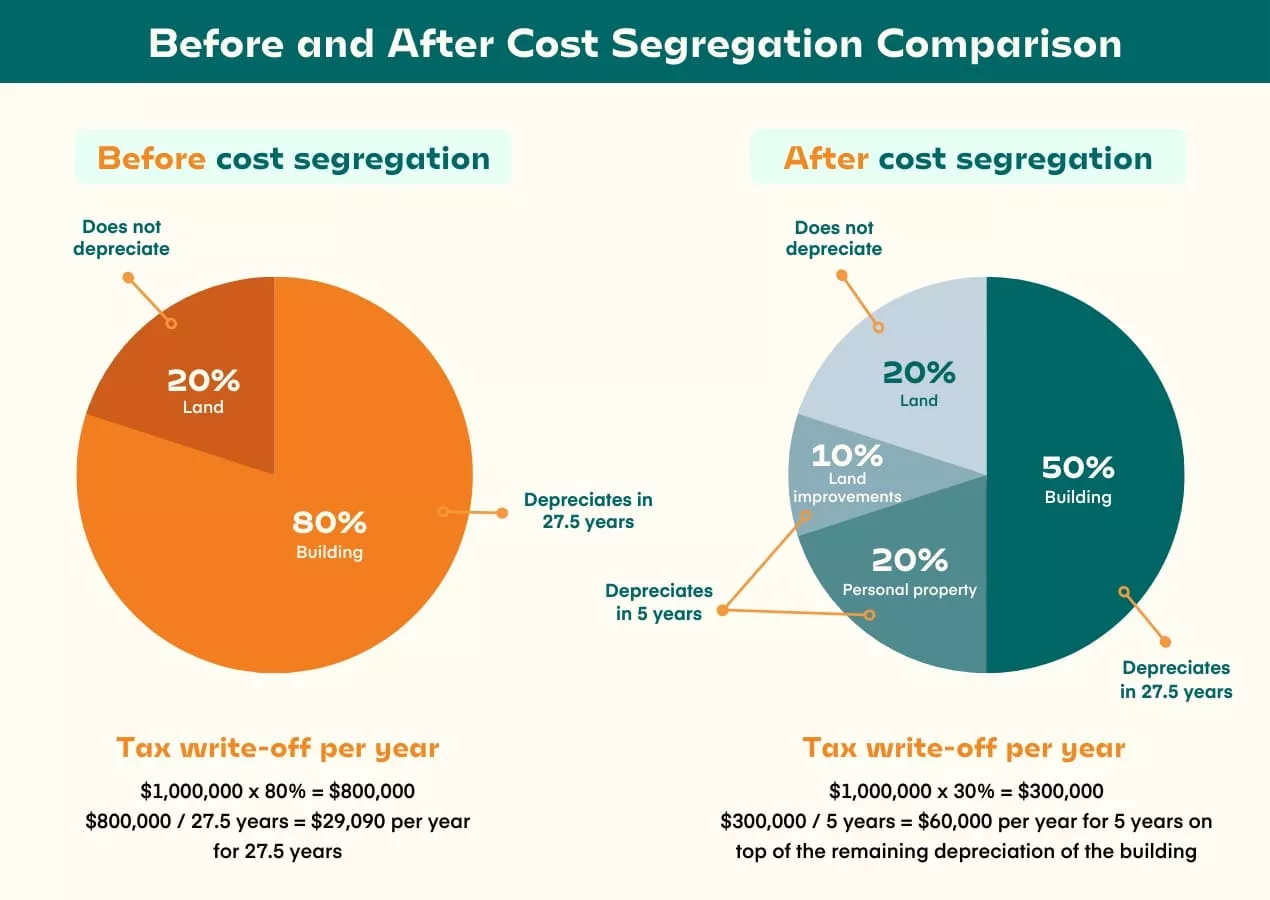

Cost Segregation Studies, which analyze the components that make up the building and assign these various components with recovery periods, can provide property owners with distinct tax advantages over the straight-line depreciation method. This system allows you to speed up the depreciation schedule, increasing the amount you can deduct each year which could mean a savings of more than 20% on taxes for the depreciation of the non-permanent, non-structural assets of their commercial investments. Currently, the rate of depreciation for real commercial property is 39 years. The purpose of a Cost Segregation Study, then, is to separate the personal property assets from the real property assets and identify and properly classify the non-structural systems and components of a commercial property so that, under IRS guidelines, the depreciation of certain qualifying assets can be accelerated to 5, 7 or 15 years instead.

Contact us now for more detailed information on a Cost Segregation Study for your investment properties.